News in review

Legislation update

Two new consumer protection reforms come into play

Two new reforms will ensure that consumers are treated fairly and ethically by financial product advisers, the Federal Government (Government) claims.

The Design and Distribution Obligations (DDO) and the Product Intervention Power should ensure that financial services products are targeted and sold to the right customers. ASIC will be empowered to intervene in instances where a product has been inappropriately sold in order to prevent harm to the consumer.

The DDO will require issuers of financial products to:

- identify target markets for their products, having regard to the features of products and consumers in those markets;

- select appropriate distribution channels; and

- periodically review arrangements to ensure they continue to be appropriate.

The minister for revenue and financial services, Kelly O’Dwyer, commented that the Product Intervention Power will enable ASIC to intervene in the distribution of a product where it perceives a risk of significant consumer detriment.

The actions ASIC could take include:

- requiring the amendment of product marketing and disclosure materials

- imposing consumer warnings and labelling changes

- restricting how a product is distributed

- banning products.

“ASIC will also be empowered to ban aspects of remuneration practices, where there is a direct link between remuneration and distribution of the product,” O’Dwyer said.

The exposure draft of the Treasury Laws Amendment (Design and Distribution Obligations and Product Intervention Powers) Bill 2018 which implements these measures, is open for comments from stakeholders until 9 February 2018.

Taxation of financial arrangements reform delayed

Simplification of the taxation of financial arrangements (TOFA) rules has been delayed. The ATO stated on its website that the TOFA rules provide the tax treatment on gains and losses of financial arrangements, and generally apply to large taxpayers.

Originally due to come into force for income years commencing on or after 1 January 2018, the reforms have been delayed until legislation passes parliament and gains Royal Assent.

The minister for revenue and financial services, Kelly O’Dwyer, blamed the delay on the Government’s “extensive legislative program”.

“Simplification of the TOFA rules is a highly complex task, and it is important to take the time to ensure that any changes are carefully considered to prevent any unintended outcomes, and to ensure the expected compliance costs savings are realised,” O’Dwyer said in a statement.

Economic update

BOJ continues stimulus policy as monetary base hits record high

In December 2017, the Bank of Japan’s (BOJ) board members voted eight-to-one to continue with its aggressive stimulus program, officially known as the “Quantitative and Qualitative Monetary Easing with Yield Curve Control” framework.

Its decision came as Japan’s monetary base increased for the 11th consecutive year to an all-time high.

The monetary base is the total amount of money in circulation and the total amount of commercial bank deposits held at the central bank. At the end of December 2017, Japan’s monetary base stood at 480 trillion yen (AU$5.4 trillion), an increase of 9.7% from 2016.

BOJ governor Haruhiko Kuroda promised to keep the stimulus going until inflation reached the target rate of 2%.

“[The bank] will continue expanding the monetary base until the year-on-year rate of increase in the observed CPI (all items less fresh food) exceeds 2 percent and stays above the target in a stable manner,” a BOJ statement said.

The short-term policy interest rate used for current accounts held by financial institutions at the bank is –0.1%.

Japan’s policy of negative interest rates increasingly stands out, as the RBA, US Federal Reserve and Bank of England are in the positive territory, with the latter two increasing rates at the end of 2017.

Japan’s long-term interest rates are also being kept accommodative, with 10-year bond yields capped at 0% and the annual pace of Japanese Government Bond purchase to remain at about 80 trillion yen (A$710 billion).

Private sector credit growth above expectations

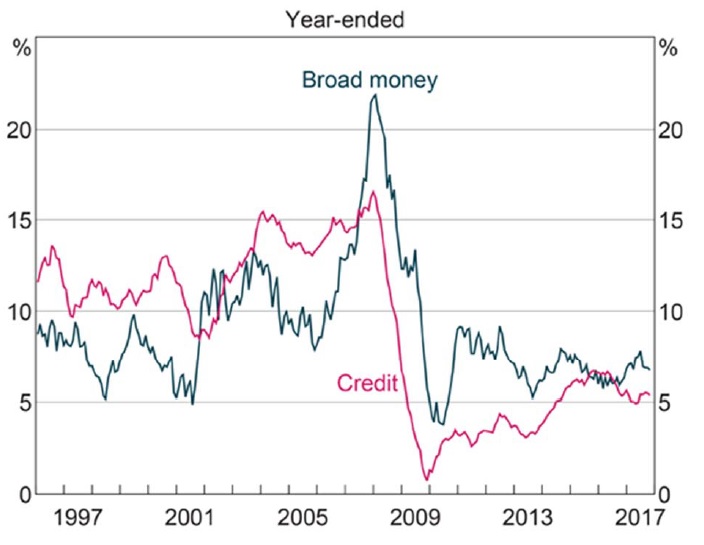

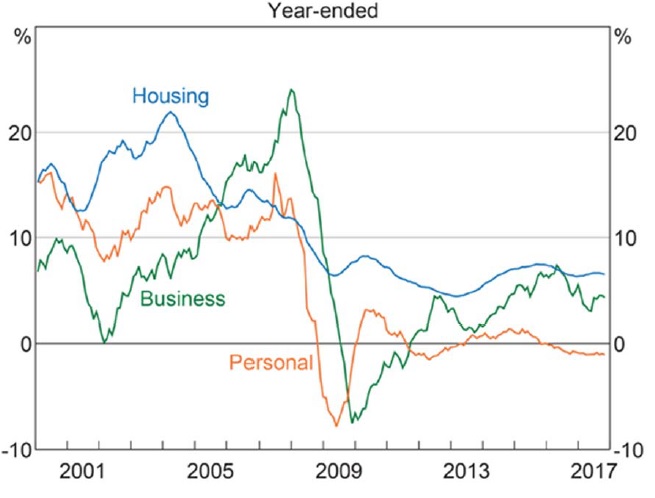

RBA data revealed that Australia’s private credit grew by 5.4% year-on-year in November, beating the predicted growth of 5.2%.

On a month-to-month basis, private credit rose by 0.5% compared with 0.4% in October. Business credit grew at the fastest pace from 0.4% in October to 0.7% in November. However, housing borrowing slowed from 0.5% to 0.4%.

On a yearly basis, housing credit rose 6.4% and business grew 4.7%. On the other hand, personal credit fell 1.2 %.

Meanwhile, the yearly growth in broad money supply slowed to 6% from 6.3% in 2016.

Figure 1: Credit and broad money growth, 1997–2017

Sources: ABS, APRA, RBA

Figure 2: Credit growth by sector, 2001–2017

Sources: ABS, APRA, RBA

Industry update

FPA reveals priorities for 2018

According to the FPA’s head of policy and government relations, Ben Marshan, The FPA has eight areas of focus for 2018.

Marshan highlighted that the key area will be lending support to the Financial Adviser Standards and Ethics Authority (FASEA).

Education standards for new financial advisers have been set, but the education standard for existing advisers has yet to be finalised, along with the code of ethics, and standards for continuing professional development.

The FPA’s other seven areas of focus are:

- assisting ASIC’s implementation of code-monitoring bodies, due to come into force on 1 January 2020

- implementation of the Australian Financial Complaints Authority — in particular, merging the three existing complaints bodies into the one new entity

- rising regulatory costs, which Marshan described as a “critical concern”

- the ASIC Enforcement Review — the recommendations from the review, due in early 2018, are expected to give ASIC the power to intervene before harm is done to customers

- renaming general advice to “product information”, and reviewing old retail/wholesale definitions — this is Financial Systems Inquiry recommendation that the Government is applying

- helping members understand and implement fintech

- the Royal Commission into Misconduct in Banking, Superannuation and Financial Services.

Insurance in Superannuation Voluntary Code of Practice a “dud”

The Government and consumer groups declared the superannuation industry’s inaugural insurance code of practice a “dud”, making regulatory intervention in the sector likely.

The Insurance in Superannuation Voluntary Code of Practice was meant to restore consumer confidence in insurance offered through superannuation, after poor claims experiences and erosion of retirement savings caused by inappropriate insurance and restrictive definitions.

Under current arrangements, members are defaulted into a range of products which can include life insurance, total, permanent disability insurance and income protection. The premiums are paid from their superannuation balance.

A draft code put out in mid-2017 was stronger, but the final code went through serious changes, one of the most important was that it became non-binding, meaning there was no obligation for a superannuation fund or insurer to adopt the watered down practices.

The code was slammed as “unenforceable” by consumer advocacy group CHOICE campaigns and policy team lead Xavier O’Halloran. Choice had spent a year consulting with the Insurance in Superannuation Working Group (ISWG) on the code.

“At the eleventh hour we’ve seen life insurers let their self-interest run rampant, creating a dud code that we cannot get behind,” O’Halloran said.

“Super funds are under a duty to act in the best interest of members, but the extreme pressure applied by the life insurers is putting that duty under serious threat … If progress is to be made, it needs to be handed over to an independent review.”

The minister for revenue and financial services, Kelly O’Dwyer, was also scathing.

“The Government is concerned that the superannuation industry has walked away from a commitment to a more robust, mandatory code of practice that had been the subject of earlier consultation,” O’Dwyer said in a statement to the ABC.

“The Government will consider an appropriate regulatory response in light of the industry’s position.”

Both the insurance companies and the superannuation funds argue that default insurance provides benefits to members who otherwise may not be covered by insurance at all.

The Government is also supportive, in principal, of default insurance being offered through superannuation.

Members of the ISWG include the Australian Institute of Superannuation Trustees (AIST), the Association of Superannuation Funds of Australia (ASFA), the Financial Services Council (FSC), Industry Funds Forum (IFF) and Industry Super Australia (ISA).

FSC finalises life insurance APL standard

The FSC has finalised its standard for life insurance approved product lists (APLs).

It is mandatory for full members of the FSC to comply with its standards, with this latest addition coming into force from 1 July 2018. APLs assist advisers and licensees because products on the list have been assessed as suitable.

According to the FSC, this standard supports “APL construction practices that promote competitive access and choice for advisers and their clients”.

It requires that APLs contain a choice of at least three life insurance providers and to be supported by robust off-APL processes that allow advisers to access other products.

“To ensure consumers have full transparency to make an informed choice, disclosure of the number of products and providers on the life insurance APL will also be included in the advice process,” the FSC said in a statement.

The standard will be reviewed within 18 months of commencement.

Superannuation funds’ financial advice offering grows

AustralianSuper is moving to goals-based advice, with the change expected to be rolled out in the first half of 2018. The fund has more than $120 billion in funds under management and 2.2 million members.

“We have to fundamentally shift our core approach to help and advice. The development of a goals based digital platform will provide members with a single view across all their financial assets and allow them to set and track their financial goals,” AustralianSuper group executive, member experience and advice, Shawn Blackmore, said in a blog post on LinkedIn.

He added the move would take the fund’s offering from a basic reactive proposition to “one that will proactively help, educate and guide members to achieve comfort, confidence and adequacy in retirement”.

The fund will also pilot the use of artificial intelligence in providing support to members, through the use of chat bots.

Market regulators’ reports and guidance

ASIC warns about inside information in sell-side research

ASIC has issued guidance that compels AFS licensees to manage conflicts of interests and inside information when providing sell-side research.

Regulatory Guide 264 Sell-side research (RG 264) gives greater clarity about how to manage conflicts of interest in the key stages of capital raising, including the preparation and production of investor education reports.

The guidance states that in the course of their work, research analysts regularly interact with and obtain information from companies, and that there is a risk that the information may be inside information.

In addition, the AFS licensees’ interests may conflict with those of investors (including potential clients), which, if not properly handled, could negatively affect the integrity of the market.

ASIC commissioner Cathie Armour explained that it was critical that that sell-side research represents the genuine, professional opinion of analysts.

“Wholesale investors want early information and analyst insights on companies undertaking capital raising. Firms that manage this process must manage the conflicting interests of their issuing and investing clients when preparing investor education research,” she said.

“It is important that this deal-related research does not undermine the prospectus disclosure or continuous disclosure requirements. RG 264 will help industry strike the right balance between these competing considerations.”

RG 264 supplements Regulatory Guide 79 Research report providers: Improving the quality of investment research (RG 79). It was issued because of uneven market practices that had developed since RG 79 was released.

The industry has until 1 July 2018 to make sure their compliance measures meet the regulators updated expectations.

Quicklink

To download RG 264, visit www.asic.gov.au:

- Select “Regulatory resources”

- Under “Find a document”, select “Regulatory guides”

- Select “RG 255–RG 264”

- Select “RG 264 Sell-side research”.

Board of Taxation chair reappointed

Michael Andrew has been re-appointed for a further two years as the part-time chair of the Board of Taxation, from 1 January 2018.

Dr Mark Pizzacalla and Craig Yaxley have also been reappointed as part-time members of the board for a further three-year period.

The board is an independent, non-statutory body that advises the government about the development and implementation of taxation legislation and the ongoing operation of the tax system.

As such, its views play an important role in how the government approaches taxation.

Andrew was chair and CEO of KPMG International from May 2011 to July 2014 and chair of KPMG Australia from 2007 to 2011. He is also a former member of the Business Council of Australia and the International Business Council of the World Economic Forum.

Board of Taxation members as of 1 January 2018 are:

- Mr Michael Andrew AO, chair

- Ms Karen Payne, CEO

- Dr Julianne Jaque, member

- Mr Neville Mitchel, member

- Dr Mark Pizzacalla, member

- Mrs Ann-Maree Wolff, Member

- Ms Rosheen Garnon, member

- Mr Craig Yaxley, member

- Mr John Fraser, ex-officio member

- Mr Chris Jordan AO, ex-officio member

- Mr Peter Quiggin PSM, ex-officio member.