Spotlight on culture; conduct in 2018

Culture under the microscope

APRA recently noted that the “issues of governance, culture and accountability in a large financial institution are complex and interwoven”. However complicated, it is a subject that will be getting plenty of media attention in 2018 due to commencement of a Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, the Bank Executive Accountability Regime (BEAR) legislation set to become law, and the Financial Adviser Standards and Ethics Authority (FASEA) developing an industry code of ethics.

While some financial advisers believe several years of scrutiny as part of the FOFA reforms and the ongoing process of becoming a profession should largely exempt them from further examination, there are no guarantees this will be the case. Indeed, the broader discussion around corporate culture and its impact on conduct has increased exponentially around the globe since the GFC, and regulators have progressively focused on the importance of a good risk culture and strong governance frameworks.

A good practice guide

Launched in December last year by Chartered Accountants Australia New Zealand, The Ethics Centre, the Governance Institute of Australia and the Institute of Internal Auditors – Australia, Managing Culture: A Good Practice Guide concedes that there are no easy answers as regulators grapple with the issue of culture and how best to monitor it. Speaking at the launch event, ASIC commissioner John Price explained that the regulator’s interest in culture is linked to its mandate as it primarily relates to conduct.

“This should not surprise anyone — ASIC is a conduct and disclosure regulator. Importantly, ASIC sees culture as a key driver of behaviour within the business community. Other strong influences on behaviour include remuneration structures and the likelihood and consequences of being caught doing the wrong thing. All of these matters are of keen interest to us as a regulator,” he said.

However, ASIC has also taken the view that “culture is not something we want to regulate with black-letter law”.

“We know it isn’t feasible to check over every company’s shoulder to test their culture, or dictate how a business should be run. But as the corporate regulator, we see the very real impact of poor culture through misconduct, scandals and poor outcomes for investors and consumers,” Price said.

Why culture matters to business

According to ASIC, companies should be interested in culture because studies have found that a good culture is best for business and for generating long-term shareholder value.

“Good culture enhances brand loyalty and bolsters reputation, which has a very real financial impact. Organisational culture can either support or damage the relationship between a company and its customers,” Price said.

For its part, APRA has also taken a direct interest in culture, linking it to the governance and risk management responsibilities of boards. In an APRA document, Information Paper: Risk Culture, released in October 2016, the regulator stated that:

In combination, a poor risk culture and weak risk management (the former often being the root cause of the latter) led to unbalanced and ill-considered risk-taking, to significant losses and, in some cases, to institutional failures. The impact on the financial stability of affected countries was significant.

APRA, as part of its Prudential Standard CPS 220 Risk Management requirements, directs boards to define the institution’s risk appetite and establish a risk management strategy.

Consider

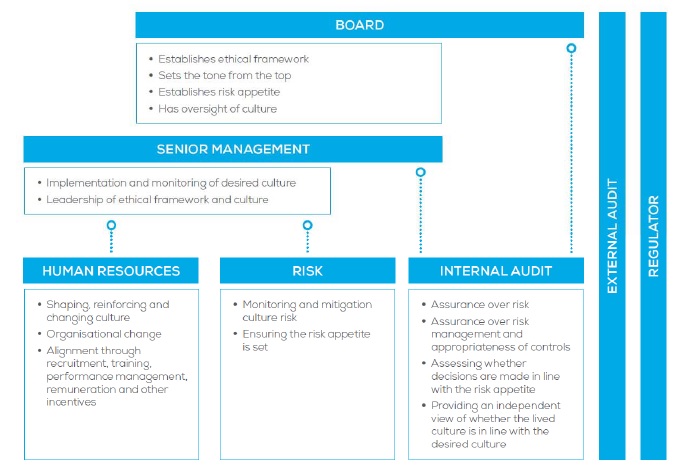

Setting and embedding a clear ethical framework is not just the role of the board and senior management — all areas can play a role:

- The board is responsible for setting the tone from the top. The board should set the ethical foundations of the organisation through the ethical framework. Consistently, the board needs to be assured that the ethical framework is embedded within the organisation’s systems, processes and culture.

- Management is responsible for implementing and monitoring the desired culture as defined and set by the board. It is also responsible for demonstrating leadership of the culture.

- Human resources (HR) is fundamental in shaping, reinforcing and changing corporate culture within an organisation. HR drives organisational change programs that ensure cultural alignment with the ethical framework of the organisation. HR also provides alignment to the ethical framework through recruitment, orientation, training, performance management, remuneration and other incentives.

- Internal audit assesses how culture is being managed and monitored, and can provide an independent view of the current corporate culture.

- External audit provides an independent review of an entity’s financial affairs according to legislative requirements, and provides the audit committee with valuable, objective insight into aspects of the entity’s governance and internal controls including its risk management.

Source: Managing Culture: A Good Practice Guide.

Figure 1: Managing culture: a good practice guide

Source: Managing culture: a good practice guide.

The big picture

In 2004, William C. Dudley, the current president of the Federal Reserve Bank of New York and a vocal proponent of improving the culture at big banks, acknowledged there had been ongoing occurrences of serious professional misbehaviour, ethical lapses and compliance failures at financial institutions in the US.

“The pattern of bad behaviour did not end with the financial crisis, but continued despite the considerable public sector intervention that was necessary to stabilise the financial system,” he said in speech in late 2014.

“As a consequence, the financial industry has largely lost the public trust. I reject the narrative that the current state of affairs is simply the result of the actions of isolated rogue traders or a few bad actors within these firms. As James O’Toole and Warren Bennis observed in their Harvard Business Review article about corporate culture: ‘Ethical problems in organisations originate not with ‘a few bad apples’ but with the ‘barrel makers’. That is, the problems originate from the culture of the firms, and this culture is largely shaped by the firms’ leadership. This means that the solution needs to originate from within the firms, from their leaders.”

It is an analogy that resonates with Australian proponents of a Royal Commission which has the power to review the suitability and effectiveness of legislation, as opposed to ASIC and APRA who can only review bank conduct within the scope of existing laws. However, the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry is just one of several measures being applied to the sector.

Royal Commission into misconduct

The Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry was established on 14 December 2017 with the commissioner, Kenneth Madison Hayne AC QC, tasked with submitting an interim report no later than 30 September 2018 and a final report by 1 February 2019. The Royal Commission’s initial public hearing was held on 12 February. But what can this inquiry realistically hope to achieve?

According to Claire Wivell Plater, managing director of The Fold Legal, much will depend on the skill of the people working with the Royal Commission and their ability to look at the underlying causes.

“I think what needs to be examined is what is giving rise to these behaviours in institutions. What systems are at play and what structures are at play that lead to this preponderance of unethical conduct. If they can get to the heart of that, then we might get some answers that might then be the genesis for change and that would be a wonderful thing,” she said.

A recent ASIC review of financial advice found a number of conflicts of interest within some of the largest vertically integrated financial institutions, with the wealth management arms of ANZ, CBA, NAB, Westpac and AMP showing a clear weighting towards in-house products in adviser recommendations.

The review found that, overall, 79% of the financial products on the firms’ APLs were external products and 21% were internal or ‘in-house’ products. However, 68% of clients’ funds were invested in in-house products.

“I think there are a number of ways that banks could address this. One would be for them to acknowledge what is relatively widely known to be true, and that is, that it’s a vertically integrated business, and regardless of the mechanism used for it, the financial planning businesses are rewarded on the contribution that they make to the overall business. I think that most planning organisations and planners within the large banks would know pretty clearly that that was what was expected of them, despite any denials of that,” Wivell Plater said.

However, ASIC has noted that vertical integration can provide economies of scale and other benefits to both the customer and the financial institution. Consumers might choose advice from large vertically integrated firms because they seek that firm’s products due to factors such as convenience and access. In this situation, recommendations of ‘in-house’ products may be appropriate. It is a point taken up by Steve Clark, director, advisory at KPMG Australia.

“I think vertical integration poses some real challenges for organisations, but it’s important to keep in mind that it’s not necessarily to the detriment of consumers,” he said.

“Outside wealth, for instance, I recently refinanced my home and in one conversation was able to deal with my mortgage, my home and contents insurance, my vehicle finance and my personal lending. That’s a lot easier for me as a consumer than running around to two or three different institutions. The issues with vertical integration often stem from product complexity, cross-subsidisation and legacy product portfolios. These are the real challenges that organisations will have to look into.”

Consider

Applying good governance

Governance means the method by which an organisation is run or governed, over and above its basic legal obligations. Governance can be argued to have four key components:

- Transparency — being clear and unambiguous about the organisation’s structure, operations and performance, both externally and internally, and maintaining a genuine dialogue with, and providing insight to, legitimate stakeholders and the market generally.

- Accountability — ensuring that there is clarity of decision-making within the organisation, with processes in place to ensure that the right people have the right authority for the organisation to make effective and efficient decisions, with appropriate consequences for failures to follow those processes.

- Stewardship — developing and maintaining an enterprise-wide recognition that the organisation is managed for the benefit of its shareholders/members, taking reasonable account of the interests of other legitimate stakeholders.

- Integrity — developing and maintaining a culture committed to ethical behaviour and compliance with the law.

As embodied in Governance Institute’s definition, good governance encompasses not only the system by which organisations are controlled, but the mechanisms by which organisations and those who comprise them are held to account. Governance, therefore, is vital to making the right decisions.

Source: Governance Institute of Australia, n.d.

Did you know?

ASIC will continue to consult with the financial advice industry (and other relevant groups) on a proposal to introduce more transparent public reporting on APLs, including where client funds are invested, for advice licensees that are part of a vertically integrated business.

ASIC noted that any such requirement is likely to cover vertically integrated firms beyond those included in this review — ANZ, CBA, NAB, Westpac and AMP. The introduction of reporting requirements would improve transparency around management of the conflicts of interests that are inherent in these businesses.

Changing culture

While the regulator has suggested that culture can be changed by focusing on things like remuneration structures, conflicts of interest, complaints handling, treatment of whistleblowers and timeliness of reporting breaches, Clark argues that culture is best understood across three ‘layers’.

“The issues identified by ASIC — remuneration, whistleblowing, management of conflicts — are all very important, but culture runs deeper,” he said.

“When we talk to clients about culture, we encourage them to consider three layers. Firstly, the artefacts of the organisation; the processes, the systems, the policies. Second layer, the espoused beliefs of the organisation; the official narrative around vision and values and the unofficial version, the stories told at the water cooler. The third layer is the beliefs and assumptions of individuals in that organisation. This is the hardest to understand and the hardest to change. In financial services today, we see many good examples of culture change initiatives. Too often though they point to solutions for an individual problem rather than considering how the organisation functions as a system and dealing with the three layers.”

The BEAR and the maiden fair

Australia looks set to follow overseas markets with government fast-tracking its Banking Executive Accountability Regime (BEAR), which will hold senior managers within banks personally accountable for their actions and those of their staff, should something in their area go wrong. However, the UK’s Senior Managers Regime and Hong Kong’s Managers-in-Charge measures have both proved controversial as the balance shifted from corporate to individual accountability. The UK legislation also began by targeting bank executives before being broadened to cover all senior managers in Britain’s financial services industry.

Some have argued that the BEAR legislation will blur the lines of responsibility between APRA and ASIC — with APRA responsible for the BEAR supervision. Wivell Plater also held some reservations.

“If somebody has been individually instrumental in the creation of a system of work that has caused systemic problems in the community, and they’ve done so knowingly … then yes, I think there’s potential for a justifiable case to hold those people individually accountable,” she said.

“Personally, I think that it’s the system of management in organisations and the way that reward structures and KPIs [key performance indicators] are established that is probably more the cause and where attention also needs to be directed.”

Under the BEAR legislation, APRA will be empowered to seek substantial fines, more easily disqualify individuals and ensure banks’ remuneration policies result in financial consequences for individuals. Banks will be required to register their senior executives and directors (accountable persons) with APRA and provide greater clarity regarding their responsibilities. However, Clark argued that BEAR in its current form affects a relatively small population of senior leaders and directors within financial institutions.

“The devil is in the detail in terms of how these impacts cascade through the organisation. There’s a high road where organisations will use it as an opportunity to address ambiguities and improve processes and a low road where organisations may simply choose to try and paper over those problems in their organisations. Organisations that choose the high road have more to gain,” he said.

In terms of the UK regulatory framework, the Senior Manager Regime sits atop at a broader regulatory framework involving the certification regime and the conduct regime. The certification regime impacts many thousands of individuals in large financial institutions. While there are potentially benefits associated with the BEAR regime, it is unclear what benefits would stem from rolling out changes comparable to the UK’s certification regime.”

Did you know?

For large authorised deposit-taking institutions (ADIs), the BEAR will commence on 1 July 2018, as Treasurer Scott Morrison believed it important to ensure that “accountability gaps in the sector are addressed as soon as possible”. For small and medium ADIs, the regime will commence from 1 July 2019, allowing them more time to comply.

Consider

The role of the board

According to ASIC, a company’s board, senior executives and management play a critical role in relation to culture and conduct. The board plays a role in setting the tone, influencing and overseeing culture, and ensuring the right governance framework and controls are in place.

Of course, for directors who are not involved in the daily operations of a company, monitoring culture can be challenging. Boards may consider the following questions to gain insights into a company’s culture, raise issues and encourage a more positive corporate culture:

- Has the culture of the organisation been independently assessed? Do the firm’s stated values match the actual experiences of customers, employees, suppliers etc.?

- Is culture a regular feature on the board and audit committee agenda?

- Do directors have broader interaction across the organisation (e.g. not limiting themselves to the chief executive officer and executive management)?

- Do directors have relationships with key employees (e.g. line managers) to gather insights about the company’s culture and issues?

- Does the board engage with external stakeholders such as customers, suppliers, and regulators?

- Is data captured on key indicators (e.g. employee feedback and surveys, customer complaints, progress on employee training on culture issues)? Is this data monitored to see how the various indicators change or move together?

- Is the information in internal and external audits being fully used?

Source: Price, 2017.

Advice underpinned by an ethical framework

How then should financial advice practices or licensees to go about balancing the inevitable tensions that arise, such as managing the profit line versus the customers’ needs, when running a business?

“The answer is a simple one, but it’s incredibly difficult to execute. All businesses involved in advice can of course profit at the expense of their customers. They can inflate the work that they do. They can make recommendations that are designed to provide remuneration for them on an ongoing basis,” Wivell Plater said.

“But at the end of the day, good sound businesses are those who have their customers’ interests at heart and who genuinely work in the interests of their customers, because they’re the businesses who will get repeat business and will be sustainable long term.”

Wivell Plater added that her legal practice often hears from financial advice businesses who need a reminder of their role in advising the client.

“One of the things we find is they’re often quite paternalistic. They feel that they have to make a recommendation to the client rather than give the client a series of options and allow the client to make decisions for themselves,” she said.

“If there was one change that I would recommend for financial planning practices it would be focusing more on options for clients and explaining the implications of those options … as long as they appropriately document what the options are, how they operate for the client and allow the client to make those decisions based on their own understanding of the position and their own preferences, then I think they could protect themselves a lot better from some of the problems that have arisen.”

Traditionally, it has taken a long time to understand and shift cultures. However new tools are becoming available that integrate insights from organisational psychology, behavioural economics and cognitive computing.

“With these tools, organisations can understand at a far more granular level what motivates and drives their employees. Armed with this understanding, leaders can implement a much more targeted and precise culture of interventions which should improve the pace of cultural change,” Clark said.

Conclusion

While organisational culture is hard to objectively assess and cannot be regulated with “black-letter law”, its role in misconduct, scandals and poor outcomes for investors and consumers has attracted government and regulatory scrutiny. Deficiencies in institutions’ attitudes towards risk are likely to be very publically addressed in 2018.

References

Australian Prudential Regulation Authority 2016 (APRA), Information Paper: Risk Culture, October,`APRA, Sydney.

Australian Securities and Investments Commission 2017,

Chartered Accountants Australia New Zealand, The Ethics Centre, Governance Institute of Australia and Institute of Internal Auditors – Australia 2016, Managing culture: a good practice guide, December.

Governance Institute of Australia (n.d.), “More thoughts on governance”, web page, Governance Institute of Australia, Sydney, viewed 22 February 2018 from <https://www.governanceinstitute.com.au/knowledge-resources/governance-foundations/more-thoughts-on-governance/>.

Dudley, WC 2014, “Enhancing Financial Stability by Improving Culture in the Financial Services Industry”, Remarks at the Workshop on Reforming Culture and Behavior in the Financial Services Industry, Federal Reserve Bank of New York, 20 October, viewed 22 February 2018 from <https://www.newyorkfed.org/newsevents/speeches/2014/dud141020a.html>.

Price, J 2017, Outline of ASIC’s approach to corporate culture, speech by John Price, commissioner, ASIC delivered at AICD Directors’ Forum: Regulators’ Insights on Risk Culture (Sydney, 19 July, ASIC Sydney.