Alternative retirement solutions to annuities

Getting the retirement solution mix right

Annuities have recently gained the most amount of attention in relation to retirement income, but even lead providers of the product acknowledge that other products will be needed for retirees to achieve good financial outcomes.

How best to provide retirement income comes as the superannuation system approaches maturity, with the focus of industry, regulators and Federal Government (Government) switching from accumulation to de-accumulation (retirement).

Did you know?

“De-accumulation” is a misnomer. While a person will commonly run down their money through retirement — thereby de-accumulating — it is possible for someone with a large account balance and savvy investment choices to end up with more assets in superannuation at their death than when they retire.

In late 2014, the Financial System Inquiry recommended that comprehensive income products for retirement (CIPRs) be developed for retiring Australians. According to retirement modelling, a CIPR could improve a retiree’s financial outcome by 15–30%.

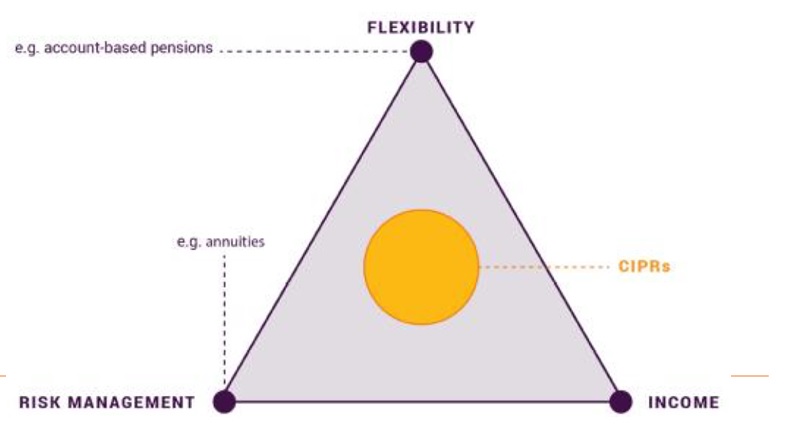

A CIPR would have three elements that need to be balanced: it needs to provide flexibility so that a lump sum can be accessed; risk management so that a broadly consistent real income can be had across the rest of a person’s life; and deliver an income that exceeds what could be achieved if all funds were fully invested into an account-based pension and drawdowns were at the minimum rate.

Figure 1. Defining a CIPR

Source: The Treasury 2016.

“[The superannuation system] has $2.6 trillion now and it’s that retirement phase that’s under-developed. The Government sees its role as providing a framework, not mandating, but giving a little bit of a nudge to the industry,” Treasury’s retirement income policy division’s Robert Jeremenko (division head), said.

Treasury wants to rebadge the unwieldly name of “CIPR” to “MyRetirement”, in part to indicate that it is related to MySuper. That is, the no-frills, default products in the accumulation phase.

However, there are differences between MySuper and MyRetirement, with the main one being that the latter is not a hard default, but rather it will require a person to opt in.

While the financial services industry is in broad agreement about the need for MyRetirement products, there is a diversity of views about how this should be done, as seen by the variety of positions taken in response to Treasury’s consultation on the matter.

Jeremenko added that there had been confusion over the term “mass customised product” and whether that meant one product for everyone with no changes allowed.

“Certainly, the Government is keen to have some sort of a default mass customised in a sense that it is a product that someone may well be offered, but if they want to take further advice either from their fund or through a financial adviser, they could have a product that was more tailored to their needs. So, the ability to have more than just one cookie cutter type product came through very strongly,” he said.

In 2016, Treasury’s then head of the retirement income policy division, Jenny Wilkinson, told delegates at the Committee for Sustainable Retirement Incomes Leadership Forum that CIPRs were not intended to:

- encourage annuities over other products

- compel individuals to take longevity products

- eliminate bequests from super

- replace the need for financial advice.

There are currently three products and strategies most utilised in retirement income, though it is hoped that more will become available when the MyRetirement framework is formalised. Industry players, such as UniSuper, have paused development until the regulatory framework firms up.

The three products/strategies that are used under current legislation are account-based pensions (ABPs), pooled investments and the bucket strategy.

ABPs

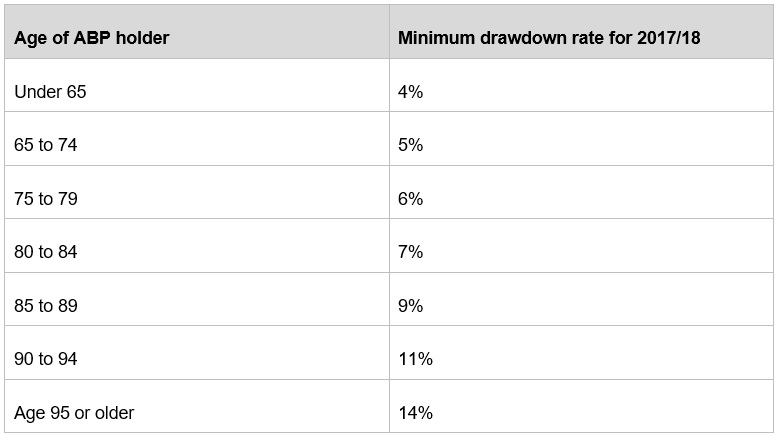

ABPs are the most popular product, with 94% of retirees having one. It is a very simple product, with the capital typically sitting in a low-yielding account. For retirees aged 65–74, a minimum of 5% is required to be drawn down from the capital per year (see Table 1). It is this regular drawdown that provides an income to the retiree.

Table 1: Minimum ABP’s drawdown rates for 2017/18

“They’re extremely attractive. They’re flexible. You’ve got choice on where to invest it. Clearly there are minimum drawdown levels, but you’ve also got the opportunity of drawing more down if you need it for those unexpected expenses,” Mercer senior partner David Knox explained.

However, in an attempt to self-insure against longevity risk, that is, the risk of outliving their savings, close to 50% of retirees are drawing down only the minimum amount when they could actually afford to draw down a higher rate, and with it a better quality of life, studies from the CSRIO (Shevchenko 2016) and the Actuaries Institute found (Actuaries Institute 2016).

“For some people, that longevity protection is actually the Age Pension. That’s A-grade, gold plated longevity protection. But for those who might retire with $500,000 or more, then they need to think about other longevity protection because they want a lifestyle that’s a bit more than the Age pension,” Knox said.

“We also have to recognise that in retirement there’s a lot of what’s called heterogeneity. We’re not all the same. We might have a partner. We might own our own home. We might not. Our health might be good or poor. We might receive a bequest from a dying parent. We might not, and so it goes on.”

Pooled investments

Pooled investment products are good at guarding against longevity risk, as they will typically give a guaranteed income.

The most common pooled investment is the annuity, but other products are beginning to surface.

A standard (or immediate) annuity pays an amount every month (or every quarter) and is backed by a life insurance company. When a client purchases an annuity, what they are in fact buying is a contract. This contract promises to regularly pay the client a defined amount of money. As the client has bought a product (that is, the annuity) they no longer have access to the capital because they have used it for the purchase. One disadvantage of this is if a large capital expense arises, they cannot get the capital back from the life company.

“One of the new products that the Government is encouraging is the deferred lifetime annuity. This annuity will start not when you retire, but maybe at the age of 85. If you don’t get to 85, you don’t get any of it. If you do get to 85, of course it’s got protection. Now both those annuities are offered by life insurance companies and are, therefore, capital needs behind them under the APRA requirements,” Knox said.

The most recent product to be developed is what is termed a “group self-annuity”. No life company is involved, rather a group of people come together and pool their money so that the risk is shared across the group.

“You put part of your retirement benefit into it. If you keep living to 95 or 100, you keep getting payments from it. If you happen to die when you’re 75 or 80, you’ll leave a little bit on the table to support those who live a bit longer,” Knox said, adding that it should give better outcomes because there was not an obligation to shareholders.

At the moment, Mercer Lifetime Plus is the only product on the market. However, other players, including superannuation funds, have been looking into this space.

Knox offered the following qualification.

“On the other hand, you don’t know what the outcome is going to be because it depends on the experience of the pool, the experience of the investment markets, the mortality experience of those in the pool,” Knox said.

It was for this reason that other market participants were cautious about the use of group pooling products. While actuarial analysis can help understand risks, the unanswerable question going into the product is: is the pool going to be large enough that there is enough money left for those that survive the longest?

Case study

| The Netherlands

The Netherlands has a pension system which is sometimes described as “collective defined contribution arrangement”. The system is a halfway house between a defined contribution and a defined benefit scheme. “It’s a little bit like our group self-annuity type product,” Knox said. The problem the Netherlands had following the global financial crisis was that investment returns were not quite as good as expected, and they had to adjust the pension payments. In some cases, it had to be cut by 2–3%. Unfortunately, retirees were not aware this could happen, even though they had technically been told. “Having said that, the Dutch system is still pretty good on the world scale. But it’s really important that people understand the expectations of what the scheme delivers and what it doesn’t deliver,” Knox said. |

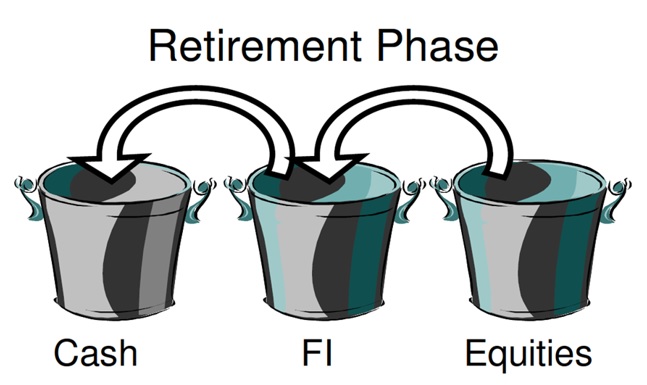

Bucket strategy

The bucket strategy is a popular tool used by financial advice firms and superannuation funds, such as State Plus and Australian Catholic Super, to help clients manage retirement income.

Typically, three ‘buckets’ of capital are set up, each serving a different purpose, with the overall objective being to provide a client a smooth flow of income while guarding against longevity risk.

One bucket is for investment in growth assets. Another is for defensive or fixed-income assets. The third is the cash bucket from which an income is drawn.

As the lion’s share of returns in superannuation is often made after a client retires, moving all of the money into a conservative option will likely lead to a reduced outcome for the client.

“In a typical lifetime, 55% of your retirement income comes from your investments after retirement. So, if you become really conservative in those years, you’ll actually hurt your retirement income,” Knox said.

Given that a client’s superannuation capital will likely be the greatest at the point of retirement, a significant part of the client’s wealth is put into the ‘growth’ bucket. The more growth there is here, the more money a client has to last them through retirement.

However, as in any well-thought-out strategy, a defensive element is also needed to generate returns through downturns in the equity and other growth markets, hence the defensive bucket.

So that losses aren’t crystallised, the client’s income is drawn from the cash bucket, which typically has two to three years’ worth of income in it. Ideally, money is moved from the growth (or defensive) bucket across to the cash bucket when the market is doing well and there are capital gains. By having two to three years’ worth of income in the cash bucket, there is time for markets to recover and losses not crystallised.

However, Knox qualified that what the bucket strategy does not take into account for the need for an immediate capital amount.

“If I suddenly need $50,000, I haven’t got enough in the cash bucket. The cash bucket is there for my regular income. I still need that capital sum, whether it’s medical expenses, dental expenses or whatever. So, the bucket strategy has real merit but it’s not the solution to everything,” he said.

Figure 2: Bucket strategy in retirement

Tax treatment of retirement income

Legislation came into effect as of 1 July 2017 to ensure that there would be no problems with the tax-free nature of a client taking a retirement income product.

However, what still remains to be sorted is how these products will affect the Social Security Age Pension test treatment.

“The Department of Social Services is currently consulting on that, and Treasury is working closely with them. That’s the remaining part of the jigsaw puzzle in terms of how all of the various aspects interact,” Jeremenko said.

Jeremenko declined to give specific dates of when a decision would be reached, as that would be decided by the Government, but indicated it was an area of focus.

Consider

| CIPR advisory group to Treasury

Minister for Revenue and Financial Services Kelly O’Dwyer announced in February that a retirement income advisory group to Treasury has been formed from nine industry and consumer experts. The experts will meet with Treasury on a regular basis for roundtable discussions. The experts are: › Mercer senior partner David Knox › Willis Towers Watson head of retirement solutions, Australia, Nick Callil › Evans Dixon managing director, head of advice, Nerida Cole › Challenger retirement income chair Jeremy Cooper › LifeCircle chair Sally Evans › SMSF Association non-executive director Deborah Ralston › UniSuper director Nicolette Rubinsztein › King & Wood Mallesons partner Ruth Stringer › Council on the Ageing chief executive Ian Yates. “That [group] will be advising Treasury on what a covenant in the SIS Act [Superannuation Industry (Supervision) Act 1993] might look like; a covenant meaning what would a super trustee be required to do in terms of examining viability of one of these super products for members,” Jeremenko said. One of the issues that has prevented the development of retirement income products is what legal ‘safe harbor’ provisions would be provided for trustees that offer them. The nature of creating a mass-customised product means that it won’t be suitable for everyone and, as such, trustee are nervous about having legal action taken against them by those it is not best suited for. “In my view, for instance, somebody with $250,000 versus someone with $600,000 versus $1 million plus are in very different situations and, therefore, their retirement product should be different. I’ve always argued that a fund should be able to offer more than one default CIPR. Whether we get to that point we’ll wait and see,” Knox said. Jeremenko added that after a few months, Treasury will go to a full public consultation on the details of CIPRs. |

Advice for advisers

Jeremenko emphasised that financial advisers should not be afraid. There is an ongoing need for financial advice, as the Government acknowledged that retirement income products was a new space into which the industry was moving.

“I don’t think people should be worried, the reason being government is taking a slow and methodical approach. My advice would be to engage with the Government and engage with the super industry to make it clear that choice and availability of different options to people in that retirement phase is crucial,” he said.

“The fact that on a whole series of analysis and modelling retirees can increase their income in retirement between 15–30% using one of these CIPR products. I mean that’s a huge increase and that is something that does not require any payment from Government to happen. That is, just simply by finding that right mix of annuity and pension that suits the particular individual.”

Knox’s best suggestion for advisers was for them to think of all the options and look beyond superannuation.

“You’ve got to take into account what other wealth clients have: are they a home owner, non-home owner, those sorts of things. I’ll give you a very simple example on longevity. It’s a bit confronting if the adviser says ‘When do you expect to die?’ when a couple walks in. But if they ask the question, ‘Now tell me about your parents. Are they still alive? Are they in good health now?’ If both of them say ‘Mum and dad are both in their 90’s and in good health’, that’s one scenario. If they say, ‘Well mum and dad both died in their 70’s’, [that’s another scenario].

“Now, in one case you’ve clearly got longevity in the genes on the horizon. That’s not guaranteeing it, but it’s more likely. In the other case, it’s less apparent. So, I think you’ve got to take into account those personal circumstances and work from that.”

He added that while MyRetirement products would not be suitable for everyone, they should provide a good benchmark for conversations, and from this, more tailored solutions offered.

Conclusion

Currently, there are very few option when it comes to retirement income products and strategies. ABPs are by far the most popular because of their flexibility, but do not offer a guaranteed income and leave retirees open to longevity risk.

Annuities are the most common pooled investment product and provide protection against longevity risk, but do not allow access to capital nor allow for investment returns for the client. New options such as deferred annuities and group self-annuity products are beginning to emerge, but have similar limitations.

A bucket strategy allows a client to access capital growth, and thereby have more funds throughout retirement, while giving downside protection against the crystallisation of losses. But, again, access to capital to pay for large expenses is limited.

The Government is keen for MyRetirement products to be developed as according to modelling, they can improve retirement outcomes by 15–30%. As it is an important area, Treasury is taking a methodical approach to get the policy settings right. However, as nothing has been decided in that respect, the development of new products by superannuation funds and other parties has been paused until there is clear direction.

References

Shevchenko PP 2016, CSRIO-Monash superannuation research cluster, CSRIO, Melbourne.Actuaries Institute 2016, The Plan for Life, Actuaries Institute, Sydney.

The Treasury 2016, Development of the framework for Comprehensive Income Products for Retirement, 15 December, Commonwealth of Australia, Canberra, viewed 28 March 2018 from <https://consult.treasury.gov.au/retirement-income-policy-division/comprehensive-income-products-for-retirement/>.